I have four graphs that summarize what we are seeing across the fundraising arena. These come from our newest analytical report, The Single Largest Gift – Cohort Analysis (SLG-CA). I know, its name is a mouthful, but its insights are plentiful. Basically, the SLG-CA analyzes an organization’s donor trends in four SLG value groups. For this analysis, the SLG categories were:

- “A Donors” (SLG of $10,000+)

- “B Donors” (those with an SLG of $1,000-9,999)

- “C Donors” (those with an SLG of $100-999)

- “D Donors” (those with an SLG under $100)

Here are the corresponding projections for each of these donor value groups, using linear regression. They are kind of self-explanatory.

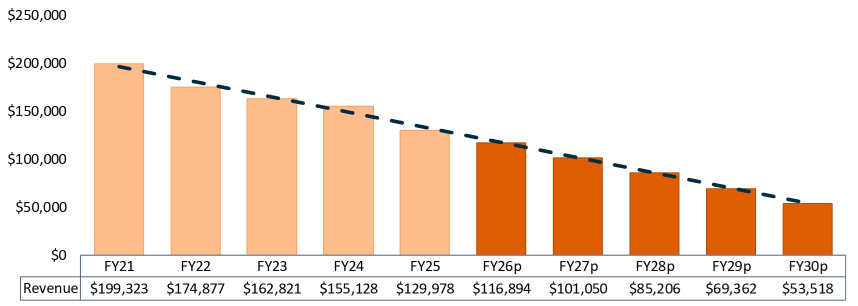

For Group D, the lowest value group, also known as General Donors:

Figure 1: Group D Donors

After peaking during the pandemic, General Donor giving has been in decline, primarily because most organizations are acquiring and retaining fewer of these donors. Fewer donors giving translates into less revenue.

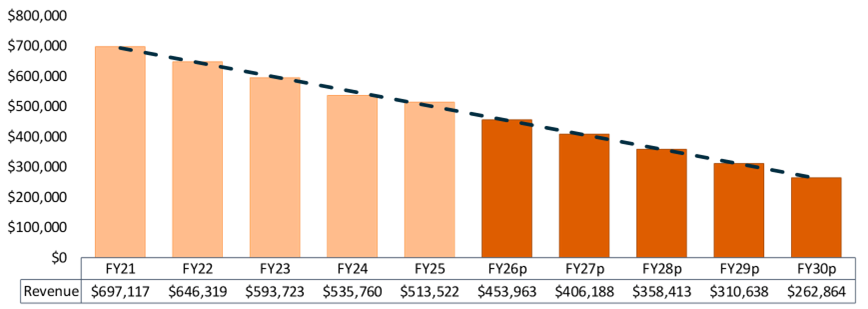

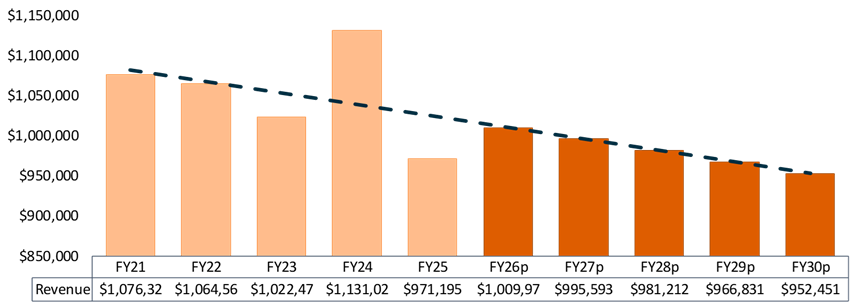

For Groups C & B, what I would call Lower & Upper-Mids, we see similar trends.

Figure 2: Group C Donors

Figure 3: Group B Donors

Group B donors do show more variation, which is typical of higher value cohorts, but overall, the trendline is downward.

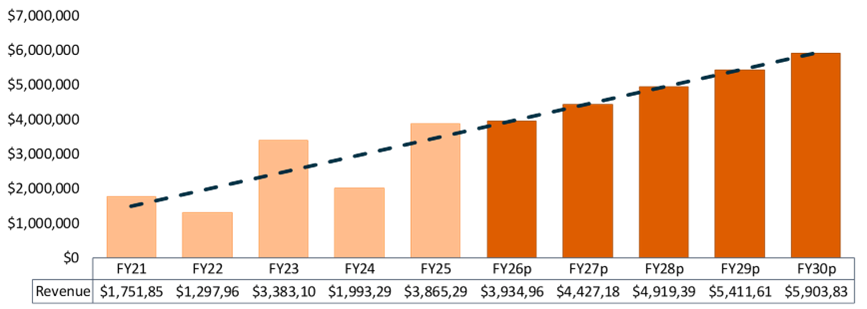

Group A, the Major Donors, are performing well, and are driving the overall revenue growth of the organization. They consist of 70% of all revenue for this organization.

Figure 4: Group A Donors

Today, more and more organizations are realizing a larger portion of their overall revenue from their Major Donors.

A couple of things about these trends:

- Organizations are placing more emphasis on the top end of their file and are being successful. A tip of the hat to those organizations.

- For this organization, 70% of its revenue is being generated by just 2% of its donors. While this profile is becoming more common in today’s fundraising environment, it does create risk as organizations are becoming more dependent on fewer donors.

- Many Major Donors don’t start out that way. A lot of Major Donors start as new General or Mid-level Donors. However, as the number of new donors declines, it does create an uncomfortable question: where will the next generation of Major Donors come from?

As I look at these trends, it feels like we are moving towards a “patron” fundraising model, which is predominate in the UK. As you look at your own donor value cohort trends, you may want to start reallocating your budget to reflect this paradigm transition.